AUTHOR : HANIYA SMITH

DATE : 21/09/2023

In today’s digital age, payment aggregators play a pivotal role in facilitating seamless online transactions. As businesses and consumers increasingly rely on electronic payments[1], understanding the nuances of a payment aggregator[2] license in India becomes essential. In this article, we will delve into the intricacies of obtaining and also operating under a payment aggregator license[3], shedding light on the regulatory framework, eligibility criteria, and key considerations.

Introduction

Payment aggregators, often referred to as payment service providers, have emerged as key players in the Indian financial ecosystem. These entities facilitate online payments for businesses and individuals, ensuring a smooth and also secure transaction experience. However, to operate legally in India, payment aggregators[4] must obtain the necessary licenses and adhere to regulatory guidelines.

Payment Aggregators in India

A Growing Industry

The payment aggregation industry in India has witnessed remarkable growth in recent years. With the increasing adoption of digital payments[5], more businesses are seeking the services of payment aggregators to streamline their payment processes.

Regulatory Bodies Governing Payment Aggregators

The Reserve Bank of India (RBI) and the National Payments Corporation of India (NPCI) are the primary regulatory bodies overseeing payment aggregators. These institutions have established guidelines to maintain the integrity of financial transactions and also protect the interests of consumers.

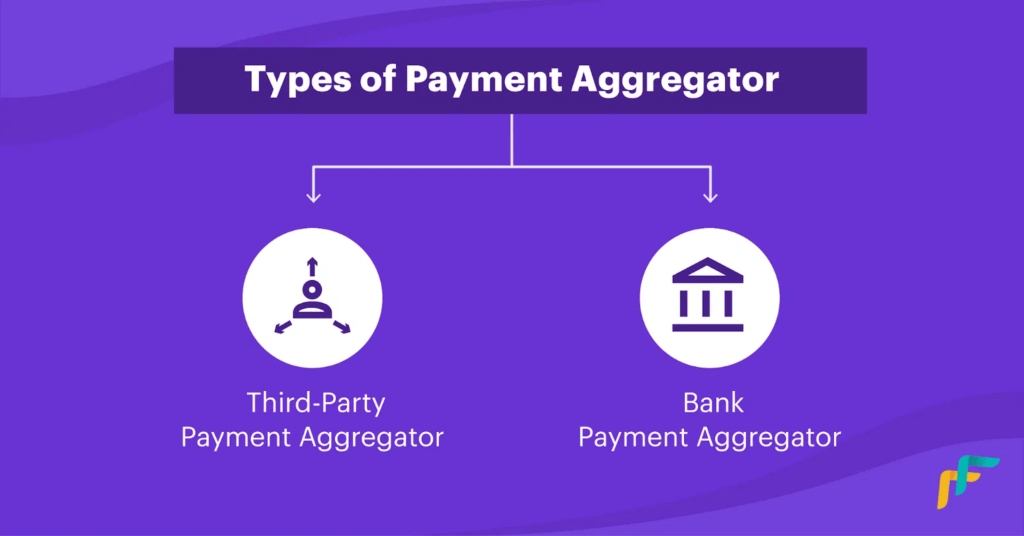

Types of Payment Aggregator Licenses

Payment aggregator licenses in India are primarily categorized into two types: PSS (Prepaid Payment System) licenses and PPI (Payment Platform for Merchants) licenses.

PSS License

PSS licenses are granted to entities that facilitate prepaid payment instruments such as mobile wallets and prepaid cards. These licenses come with specific regulatory requirements and also compliance obligations.

PPI License

PPI licenses, on the other hand, are issued to payment aggregators [1]that cater to merchants and also businesses. This license allows them to provide payment gateway services, enabling online businesses to accept payments from customers seamlessly.

Eligibility Criteria

To obtain a payment aggregator license, applicants must meet certain eligibility criteria set by regulatory authorities.

Financial Requirements

Applicants must demonstrate their financial stability and also capability to handle transactions securely. This includes maintaining a minimum net worth as specified by the regulatory bodies.

Fit and Proper Criteria

Regulators assess the integrity and competence of the individuals associated with the payment aggregator. Only individuals who meet the “fit and proper” criteria are eligible to operate under the license.

Application Process

The application process for obtaining a payment aggregator license[2] is meticulous andalso requires the submission of various documents.

Documentation

Applicants must submit detailed documentation, including business plans, financial statements, and also compliance frameworks, to prove their suitability for a license.

Timeframe

The timeframe for obtaining a payment aggregator license can vary, depending on the completeness of the application and regulatory review. It typically takes several months to secure the necessary approvals.

Compliance and Security also

Compliance with regulatory guidelines and also ensuring transaction security are paramount for payment aggregators.

Data Protection

Payment aggregators must implement robust data protection measures to safeguard customer information and also prevent data breaches.

Risk Management

Managing transactional risks is a critical aspect of payment aggregation. Implementing risk assessment protocols helps in identifying and also mitigating potential threats.

Operational Guidelines

Operating under a payment aggregator license entails adhering to specific operational guidelines.

Transaction Limits

Regulators often set transaction limits that payment aggregators[3] must adhere to, ensuring the safety of transactions for both businesses and also consumers.

Settlement Procedures

Payment aggregators must establish transparent settlement procedures to ensure timely disbursement of funds to merchants.

Challenges and Opportunities also

While the payment aggregation industry presents significant opportunities, it also comes with its fair share of challenges.

Competition

The sector is highly competitive, with multiple players vying for market share. Staying innovative and also customer-centric is crucial for success.

Market Trends

Understanding and adapting to evolving market trends, such as the rise of contactless payments and mobile wallets, is vital for sustained growth.

Case Studies

Exploring success stories and also learning from the experiences of established payment aggregators[4] can provide valuable insights for newcomers in the industry.

Future Prospects

The future of payment aggregation in India holds promise, with the industry continually evolving to meet the changing needs of businesses and consumers.

Conclusion

In conclusion, obtaining a payment aggregator license in India is a comprehensive process that requires adherence to regulatory guidelines, financial stability, and also a commitment to data security. As the digital payment landscape continues to expand, payment aggregators play a pivotal role in facilitating secure and efficient transactions for businesses and consumers alike.

FAQs

- What is a payment aggregator license?

A payment aggregator license is a regulatory authorization that allows an entity to provide payment aggregation services, facilitating online transactions for businesses and individuals. - How long does it take to obtain a payment aggregator license in India?

The timeframe for obtaining a payment aggregator license varies but typically takes several months, depending on the completeness of the application and also regulatory review. - Are there any restrictions on the types of transactions a payment aggregator can facilitate? Regulatory bodies may impose transaction limits and also guidelines that payment aggregators must follow to ensure the safety of transactions.

- What are the major challenges faced by payment aggregators in India?

Payment aggregators in India face challenges related to competition, data security, and the need to adapt to rapidly evolving market trends.

+44 7496 916610