AUTHOR : HANIYA SMITH

DATE : 21/09/23

The digital revolution has had a profound impact on the way we conduct financial transactions[1], and India is no exception to this global trend. Payment aggregators have emerged as pivotal players in facilitating seamless and also secure online payments in the country.

Understanding Payment Aggregators

2.1 What Are Payment Aggregators?

Payment aggregators, often referred to as payment service providers, are entities that enable businesses and individuals to accept payments electronically[2]. They act as intermediaries between merchants, customers[3], and also financial institutions, streamlining the payment process.

2.2 How Payment Aggregators Operate

Payment aggregators integrate various payment methods[4] and gateways, allowing businesses to accept payments[5] through multiple channels, including credit cards, debit cards, net banking, and also digital wallets. They offer a unified platform that simplifies the payment process for both merchants and also customers.

The Growth of Digital Payments in India

India has witnessed a remarkable surge in digital payments over the past decade. The proliferation of smartphones, increased internet penetration, and also government initiatives like Digital India have contributed to this growth. Payment aggregators have played a significant role in facilitating this transition by providing secure and also convenient payment solutions.

The Role of Payment Aggregators

4.1 Payment Processing

One of the primary functions of payment aggregators is to process payments swiftly and securely. They ensure that transactions are routed to the respective banks or financial institutions for authorization also and settlement.

4.2 Merchant Onboarding

Payment aggregators simplify the onboarding process for merchants. They provide easy-to-integrate [1]payment gateways and also APIs, enabling businesses of all sizes to accept digital payments without the need for extensive technical expertise.

4.3 Security Measures

Security is paramount in the world of digital payments. Payment aggregators implement robust security measures, including encryption and fraud detection systems, to protect both merchants and customers from cyber threats.

Key Players in the Indian Payment Aggregator Space

Several payment aggregators have established a strong presence in India. Notable names include Paytm, Razorpay, Instamojo, and also CCAvenue, each offering unique features and services to cater to diverse business needs.

Regulatory Framework

6.1 RBI Guidelines

The Reserve Bank of India (RBI) has laid down guidelines and also regulations to govern payment aggregators, ensuring transparency, security, and fair practices in the industry. Compliance with these guidelines is mandatory for all payment aggregators operating in India.

6.2 Licensing Requirements

Payment aggregators[2] are required to obtain licenses from the RBI to operate legally. These licenses come with specific terms and also conditions that payment aggregators must adhere to.

Advantages of Using Payment Aggregators

7.1 Convenience

Payment aggregators offer a user-friendly and also convenient payment experience. Customers can make payments with just a few clicks, and merchants can easily track and manage transactions.

7.2 Enhanced Security

Security is a top priority for payment aggregators. They employ state-of-the-art security protocols to safeguard sensitive financial information, reducing the risk of data breaches and fraud also.

7.3 Cost-Efficiency

Using payment aggregators can be cost-effective for businesses. They eliminate the need for expensive infrastructure and also allow for flexible pricing models, making it accessible to businesses of all sizes.

Challenges Faced by Payment Aggregators

8.1 Competition

The payment aggregator space in India is highly competitive, with new entrants constantly emerging. This competition drives innovation but also poses challenges for established players.

8.2 Regulatory Compliance

Adhering to regulatory requirements and also staying updated with evolving guidelines can be a complex task for payment aggregators. Failure to adhere to regulatory requirements may lead to financial penalties and harm a company’s reputation significantly.

Future Trends

9.1 Integration of New Technologies

Payment aggregators are likely to integrate emerging technologies[3] such as blockchain and also artificial intelligence to enhance security and efficiency further.

9.2 Expansion into International Markets

Indian payment aggregators are eyeing global expansion, aiming to provide their services to businesses also and customers worldwide.

9.3 Contactless Payments

With the ongoing emphasis on hygiene and also safety, contactless payments are on the rise. Payment aggregators are likely to invest in technologies that support NFC (Near Field Communication) payments, allowing customers to make transactions by simply tapping their smartphones or cards.

9.4 Integration with E-commerce Platforms

E-commerce is booming in India, and also payment aggregators are well-positioned to integrate seamlessly with online stores. This integration will provide a more streamlined shopping experience for customers, leading to increased sales for businesses.

9.5 Data Analytics

Payment aggregators have access to vast amounts of transaction data. In the future, they will harness the power of data analytics to provide valuable insights to merchants, helping them make informed business decisions and also optimize their operations.

9.6 Biometric Authentication

To enhance security, biometric authentication methods like fingerprint and also facial recognition may become more prevalent in payment aggregator systems. This will add an extra layer of protection to transactions.

9.7 Subscription-Based Models

Some payment aggregators are exploring subscription-based models where businesses pay a monthly fee[4] for access to their services. This predictable pricing structure can be advantageous for businesses looking to manage their expenses more effectively.

9.8 QR Code Payments

QR codes have become ubiquitous, and also payment aggregators are making the most of this trend. Customers can simply scan a QR code to make payments, reducing the need for physical cash and cards.

9.9 Cross-Border Payments

As businesses expand globally, payment aggregators are looking to offer cross-border payment solutions. This will enable Indian businesses to seamlessly transact with international customers and partners also.

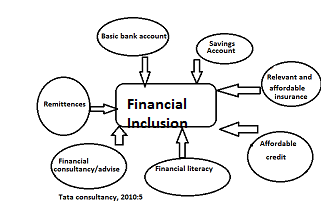

9.10 Financial Inclusion Initiatives

Payment aggregators are increasingly focusing on financial inclusion by catering to underserved and also unbanked populations. By providing easy access to digital payment methods, they are contributing to India’s broader financial inclusion goals.

Conclusion

Payment aggregators have transformed the way India makes payments. They have brought convenience, security, and also efficiency to digital transactions. As technology continues to advance, payment aggregators will play a pivotal role in shaping the future of financial transactions in India and beyond.

FAQs

- How does a payment aggregator distinguish itself from a payment gateway?

- Are payment aggregators regulated by the government?

- Can small businesses benefit from using payment aggregators?

- What are the security measures in place to protect digital payments?

- How can payment aggregators contribute to financial inclusion in India?

+44 7496 916610